Day 3: The Illusion of Stock Market Gains: Exploring Alternative Assets Like Bitcoin and Class B/C Multi-Family Real Estate

By Rodeen Rahbar, MD Board-Certified Physician and Entrepreneur in Real Estate and Wealth Creation

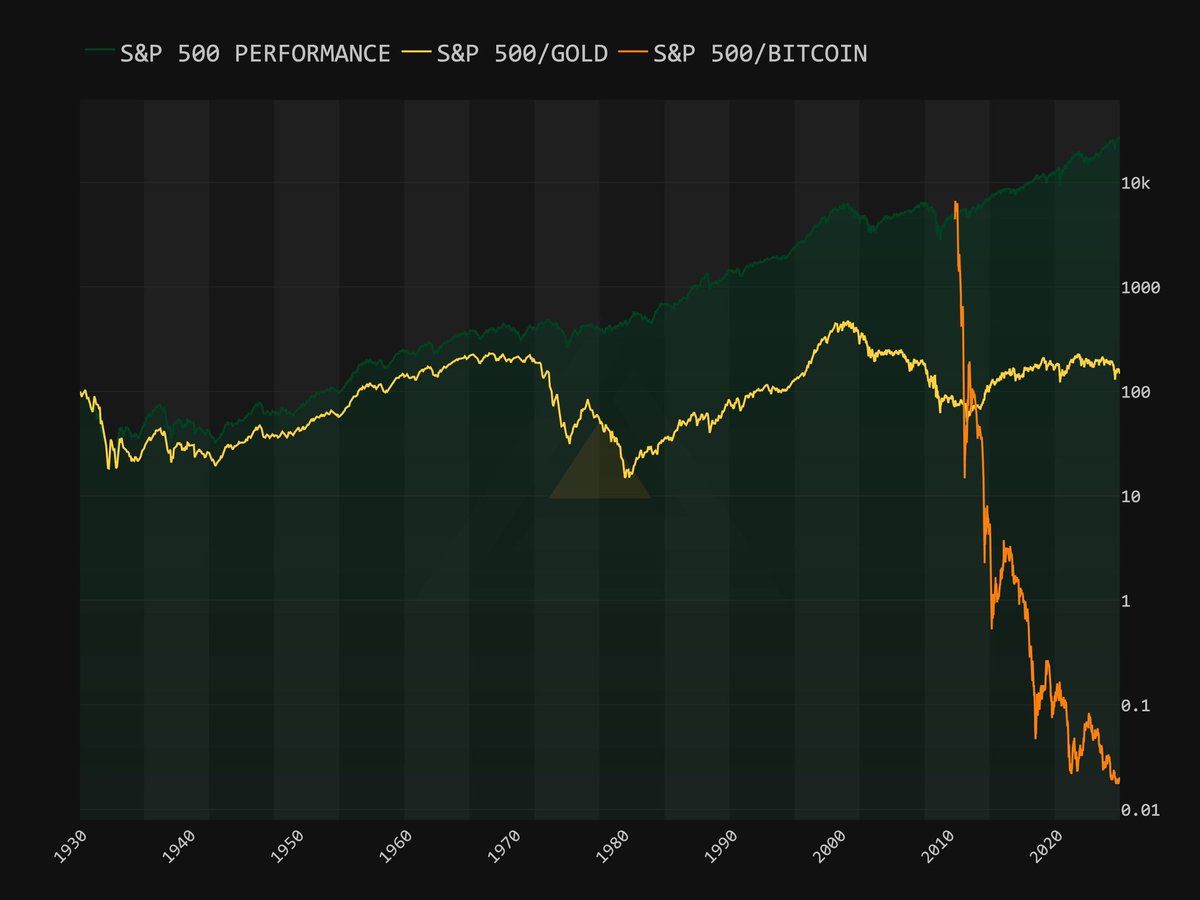

In the world of investing, the S&P 500 is often hailed as the benchmark for long-term wealth creation. Headlines frequently tout its impressive nominal gains over decades, painting a picture of relentless upward momentum. But what if those gains are more illusion than reality? A thought-provoking graph shared on X by user @Aeraryum challenges this narrative, showing that when adjusted for alternative stores of value like gold and Bitcoin, the stock market's performance tells a different story.

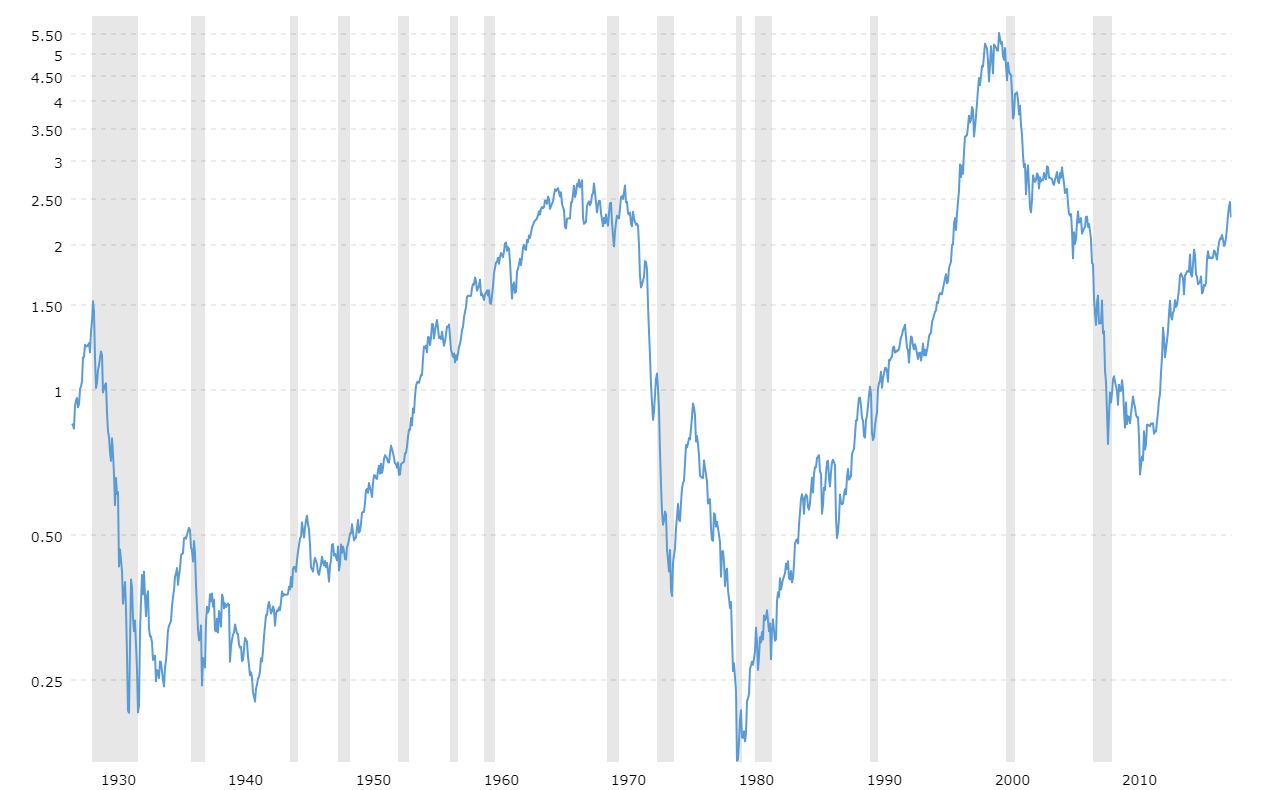

The graph above illustrates the S&P 500's nominal performance (in green) from 1930 to around 2020 on a logarithmic scale, alongside the index divided by gold prices (yellow) and divided by Bitcoin prices (orange). Nominally, the S&P 500 has skyrocketed, delivering multiplicative returns that seem unbeatable. However, the yellow line—representing S&P 500 divided by gold—fluctuates without a clear upward trend, hovering around similar levels over the long term. This suggests that much of the stock market's "growth" is simply a reflection of currency debasement and inflation, as gold has historically served as a hedge against such forces.

Even more striking is the orange line, which starts in the early 2010s when Bitcoin emerged. It begins high but plummets dramatically, indicating that the S&P 500 has lost tremendous value relative to Bitcoin. In essence, if you've been holding stocks while Bitcoin has been appreciating, your purchasing power in terms of this digital asset has eroded significantly. This graph underscores a key point: traditional equities may not be the ultimate wealth preservers in an era of fiat money expansion.

Bitcoin: The Ultimate Digital Property and Sound Money

Bitcoin stands out as a prime example of an alternative asset that outperforms in this context. Often dubbed "digital gold," Bitcoin is designed with a fixed supply of 21 million coins, making it inherently deflationary and resistant to the inflationary pressures that plague fiat currencies. Since its inception in 2009, Bitcoin has achieved annualized returns exceeding 200% in many periods, far surpassing the S&P 500's average of around 10-11% annually.

What makes Bitcoin potentially the best digital property in human history? Its role as sound money. Unlike central bank-issued currencies, which can be printed at will—leading to debasement as seen in the post-1971 era after the U.S. abandoned the gold standard—Bitcoin operates on a decentralized network secured by proof-of-work. This scarcity mimics gold's properties but adds advantages like portability, divisibility, and verifiability in the digital age.

In 2025, with U.S. national debt exceeding $35 trillion and ongoing monetary expansion, institutional adoption has surged. Bitcoin ETFs have attracted over $50 billion in inflows since their approval, and companies like MicroStrategy have made it a core treasury asset, reporting billions in fair value appreciation. As the graph shows, holding Bitcoin has not only preserved but multiplied value relative to stocks, positioning it as a hedge against systemic financial risks.

The chart above (re-created from historical data sources) depicts the S&P 500 to gold ratio, highlighting how stocks have failed to consistently outpace gold over extended periods.

Class B/C Multi-Family Real Estate: A Tangible Hedge Against Inflation

While Bitcoin represents the digital frontier, Class B and C multi-family real estate offers a more traditional, tangible alternative for investors seeking stability amid economic uncertainty. These properties—typically 20- to 40-year-old apartment buildings in working-class neighborhoods—provide steady cash flow through rentals and appreciate in value over time, often outpacing inflation.

In 2025, the multifamily sector is showing signs of recovery after a period of elevated supply. Vacancy rates for B- and C-class properties stand at around 5%, lower than the 7.8% for luxury Class A apartments. Effective rents are rising, with projections for positive growth below long-term averages, while new completions are expected to decline toward historical norms due to higher interest rates and tighter lending. Cap rates for C-class properties hover around 6.71%, offering attractive yields for income-focused investors.

Why do these assets shine? They benefit from inflation through rent adjustments—landlords can increase rents to match rising costs, maintaining real returns. Post-2020 housing shortages, fueled by underbuilding and population shifts, have pushed occupancy to 95% in many markets. Value-add opportunities, such as unit renovations, can boost net operating income by 20-30%, enhancing overall performance.

Moreover, real estate allows for leverage, where investors use debt to amplify returns, and tax benefits like 1031 exchanges enable deferred capital gains. In an inflationary environment, where nominal stock gains mask eroding purchasing power, Class B/C multifamily properties provide reliable income and capital preservation. As the Federal Reserve cuts rates in 2024-2025, borrowing costs are decreasing, making acquisitions more appealing.

Conclusion: Diversifying Beyond the Stock Illusion

The graph from @Aeraryum serves as a wake-up call: nominal gains in stocks can be misleading when viewed through the lens of sound money alternatives. Bitcoin, with its unparalleled scarcity and adoption trajectory, exemplifies digital property that thrives in debased fiat systems. Meanwhile, Class B/C multi-family real estate offers grounded, income-generating protection against inflation.

As we navigate 2025's economic landscape—with stabilizing multifamily markets and continued Bitcoin institutionalization—investors would do well to diversify into these assets. While stocks remain a cornerstone, true wealth building may lie in what preserves value, not just what appears to grow on paper.

Questions and Comments from Physicians (10/8/2025)

Following the publication of the article on the illusion of stock market gains and the rise of alternatives like Bitcoin and Class B/C multi-family real estate, several readers raised thoughtful objections. Below, I've compiled a Q&A addressing the most common ones, drawing on historical data, expert insights, and economic principles to provide balanced responses.

Q1: Bitcoin is too young to compare fairly to the S&P 500, which draws from the NYSE's 233-year history, or gold, which has been a store of value for millennia. Isn't this an apples-to-oranges comparison?

A: It's true that Bitcoin, launched in 2009, lacks the centuries-long track record of the NYSE (founded in 1792) or gold's ancient role as money dating back over 5,000 years. However, the comparison in the graph isn't about longevity but about performance as a store of value in the modern fiat era, particularly post-1971 when the U.S. dollar detached from gold. Bitcoin's youth is actually a strength: in just 16 years, it has achieved a market cap over $1 trillion and outperformed both stocks and gold in real terms during periods of aggressive money printing. The S&P 500's long history includes devastating drawdowns—like the 57% drop in 2008-2009 or the 87% crash in 1929-1932—showing that age doesn't guarantee stability. Gold has endured, but its returns have been flat relative to stocks in nominal terms over decades. Bitcoin's fixed supply and decentralized network address flaws in both, making it a valid benchmark for today's digital economy. Over time, as adoption grows (e.g., nation-states like El Salvador holding it as reserves), its "youth" may prove an advantage in adaptability.

Q2: Gold is too expensive to store and bulky, making it impractical for most investors. Isn't the S&P 500 still better for ease of access? What about options like vaulted bullion, and why might Bitcoin emerge as superior to gold in the long run?

A: Gold's physical nature does pose challenges: it's bulky for large holdings, vulnerable to theft if stored at home, and incurs ongoing costs. Professional vault storage, such as allocated or vaulted bullion in secure depositories (e.g., through companies like Suisse Gold or SD Bullion), typically costs around 0.5% of the asset's value annually, with minimum fees starting as low as $9.99 per month for smaller amounts. These options provide insured, segregated storage in facilities like those in Zurich or Singapore, offering peace of mind without the bulk at home. ETFs like GLD allow indirect exposure without physical handling, though they introduce counterparty risk.

That said, the S&P 500's ease (low-cost index funds, no storage fees) doesn't make it inherently better, as the article highlights how nominal gains erode against inflation and debasement. Gold has preserved value over millennia, but Bitcoin could surpass it long-term due to superior properties: it's digital and weightless (no storage costs beyond a wallet), infinitely divisible, transferable globally in seconds without intermediaries, and verifiable on a blockchain. Unlike gold, which can be confiscated or diluted by new mining, Bitcoin's 21 million cap is immutable. As digital economies dominate, Bitcoin's portability and resistance to censorship position it as "digital gold" upgraded for the 21st century, potentially capturing gold's $15 trillion market while avoiding its logistical drawbacks.

Q3: Short-term performance matters too— if you had invested in the S&P 500 the day before the 2008 crash, you'd still have insane returns today. Doesn't this show stocks are resilient regardless?

A: This argument relies on hindsight and perfect timing, which is rarely achievable for most investors. If you invested in the S&P 500 at its peak on October 9, 2007 (just before the crash), the index fell 57% to its March 2009 low, and it took until 2013 to recover to pre-crash levels nominally—not accounting for dividends or inflation. By February 2024, that investment would have grown about 350% in total (including reinvested dividends), which sounds impressive. However, this ignores opportunity costs: during the recovery, alternatives like gold rose over 300% from 2007 to 2011, and Bitcoin (from 2010 onward) delivered exponential gains.

The real issue is that no one can consistently time the market—missing the best days (often right after crashes) can halve long-term returns. For non-traders, who make up most investors, long-term holding is key, but even then, the S&P's average annual return of ~10% nominal since 1926 drops to ~7% after inflation. Volatility in short-term windows (e.g., intra-year drops averaging 15% over the past 20 years) can lead to emotional selling at lows. Alternatives like Bitcoin or real estate emphasize real, inflation-adjusted preservation over decades, not short-term spikes. Dollar-cost averaging into diversified assets mitigates timing risks better than betting solely on stocks' resilience.

Q4: Bitcoin technically has absolutely no utility—it's slow, expensive for transactions, and energy-hungry. There are other cryptos that are as secure but much faster and efficient, yet Bitcoin persists. How do you refute this?

A: Bitcoin's critics often focus on its transactional limitations—high fees during peaks, ~7 transactions per second, and energy consumption equivalent to a small country—but this misses its core purpose as a store of value, not a payment rail. Drawing from Michael Saylor's insights, Bitcoin isn't competing as "digital cash" for coffee purchases; it's "digital property" or "digital energy," the apex monetary asset due to its unmatched decentralization, security, and network effects. Saylor argues there's "no second best": other cryptos (e.g., Ethereum for smart contracts or Solana for speed) are more like securities or tech platforms, vulnerable to centralization, regulatory scrutiny, or founder control. Bitcoin's energy use isn't waste—it's the proof-of-work mechanism that secures the network against attacks, making it the most battle-tested blockchain with over 99.99% uptime since inception.

Its "slowness" is intentional for security; layers like Lightning Network enable fast, cheap micropayments off-chain. Persistence comes from first-mover advantage: a $1.5 trillion market cap, institutional adoption (e.g., ETFs, corporate treasuries), and immutability that no altcoin matches. Saylor emphasizes Bitcoin's scarcity as thermodynamic truth—converting energy into immutable value—outshining faster but less secure alternatives that often fail during stress (e.g., Terra's collapse). In a world of infinite fiat, Bitcoin's "utility" is being the hardest money ever created. For more on this, check out Michael Saylor's discussions on his X profile: https://x.com/saylor.

Q5: You mention Multi-Family Class B/C Real Estate as an alternative, but you don't graph its return compared to the S&P. Why not?

A: Graphing returns for Class B/C multi-family real estate against the S&P 500 isn't straightforward due to the asset class's inherent diversity and structure. There are hundreds of ways to invest in real estate—through direct ownership, REITs, syndications, or funds—each with unique factors like location, management quality, leverage, and market conditions influencing performance. Unlike the S&P 500, which is a standardized index with publicly available historical data, real estate deals are often private and heterogeneous, making apples-to-apples comparisons challenging.

Additionally, SEC rules restrict how syndicators and funds can advertise or compare performance. Regulations like those under Regulation D prohibit general solicitation of past returns in a way that could be seen as promoting specific investments, and each deal must be evaluated independently based on its merits, risks, and projections rather than historical aggregates. Aggregated indices like the NCREIF Property Index exist for multifamily real estate, showing average annual returns of around 7-10% over long periods (including income and appreciation), which can compete with or exceed the S&P's inflation-adjusted returns—but these are broad averages, not reflective of individual Class B/C deals.

Hold periods for many syndications are typically 5 years or less, focusing on value-add strategies and exits via sales or refinances, which doesn't lend itself to long-term graphing like the S&P's multi-decade charts. Attempting to plot them could mislead by implying consistency that's not there, as short-term real estate cycles (e.g., influenced by interest rates or local economies) vary widely. I don't disagree with this analysis; it aligns with the practical realities of real estate investing, emphasizing due diligence on specific opportunities over broad benchmarks. For long-term wealth preservation, the focus should be on total return metrics like IRR (internal rate of return), which for well-managed Class B/C deals often target 15-20% annually, but again, these are deal-specific.

Have comments? Let me know what you think! Click the CONTACT button at the top of this page and send me a message!!